Letters: Competition Bureau Sues Google

December 1, 2024Welcome to Letters from CAMP, a newsletter on anti-monopoly activity in Canada and abroad, brought to you by the Canadian Anti-Monopoly Project. In this installment we have:

Let's dive in.

Google’s AdTech Empire Faces Canadian ReckoningCanada’s Competition Bureau has launched a bold legal challenge against Google, accusing the tech giant of monopolizing online advertising to the detriment of Canadian businesses and consumers. The Bureau claims Google has tied its various ad tech tools together, effectively locking customers into its ecosystem while freezing out potential competitors. This follows a record-setting year in which over 200 billion Canadian ad transactions flowed through Google’s ad systems—a sobering statistic highlighting just how much influence one company can wield. This case is the Bureau’s most ambitious enforcement action in years, paralleling the U.S. Department of Justice’s high-profile litigation targeting Google’s advertising empire. It’s a critical test of Canada’s recently updated competition laws, including strengthened powers to address abuse of dominance. Notably, it’s been nearly a decade since the Bureau’s last major abuse of dominance litigation — that time it was an unsuccessful attempt to shake up the supply of in-flight meals at the Vancouver International Airport. It’s clear that today the enforcer’s ambition is better aligned with Canada’s monopoly moment. In a statement responding to the announcement, CAMP executive director Keldon Bester noted that “online advertising is a critical tool for every Canadian business trying to reach their customers, and monopolization of this market means inflated costs that are ultimately borne by consumers.” The challenge also reflects a shift in focus towards the structures and incentives that allow firms to choke off competition. With the Bureau calling for divestitures along with financial and behavioural penalties, it’s clear Canada is stepping up as an equal partner in the global pushback against concentrated power. In taking on one the largest companies on the planet, the Bureau is in for a serious fight. But it will take swings like these to deliver the benefits of competition to Canadians across the country. 📚 What We’re Reading 📚

Food Fight: Grupo Bimbo Accuses Maple Leaf of Cartel EntrapmentGrupo Bimbo has filed a $2 billion lawsuit against Maple Leaf Foods, claiming it was misled into buying a company embroiled in Canada’s infamous bread price-fixing cartel. It’s a new twist in a scandal that has already seen grocery giants like Loblaw and Weston settle class-action lawsuits while the results of the government’s case against the cartel largely remain to be seen. The story underscores the glacial pace of enforcement or accountability for the alleged participants under Canada’s competition law. Uncovered seven years ago, Grupo Bimbo is the only player so far to face any penalties from the government’s investigation. This is the case despite the cooperation of Loblaws in uncovering the cartel in the first place and their corresponding immunity deal. But justice has come from other areas of the legal system in the meantime. Loblaw and George Weston, the first defendants to settle lawsuits, agreed to pay $500 million in damages earlier this year, inclusive of the $96 million they previously distributed in $25 gift cards as compensation. Still, these settlements pale in comparison to the potential scale of the cartel conduct, which overcharged Canadian consumers an estimated $5 billion between 2001 and 2015. Despite this, many accused grocers, including Sobeys and Metro, deny participation in the scheme, arguing Loblaw’s accusations aim to shift blame from their central role. 📰 CAMP in the News 📰

Algorithmic Rent Hikes Under the SpotlightCorporate landlords are in hot water as Canada’s Competition Bureau investigates allegations of algorithmic collusion in rental markets. The Bureau’s inquiry, prompted by reports of Canadian landlords using AI tools like YieldStar, has put a spotlight on a practice some call a “housing cartel.” Designed to recommend higher-than-market rents by analyzing confidential industry data, these pricing tools have already drawn antitrust legal challenges and grassroots pushback in the U.S.. While we await the outcome of this investigation, it’s worth considering how antitrust cases can deliver a treasure trove of important revelations. Remember the bread price-fixing scandal? Emails unearthed during legal proceedings described cozy conversations between corporate executives about price adjustments for more kinds of food than just bread. Will the same happen here? What might a deep dive into landlords’ inboxes reveal about the human side of algorithmic decision-making? Some major landlords, like Dream Unlimited, have announced a pause in using YieldStar amid the scrutiny, but let’s not mistake damage control for accountability. As Canada works to reverse the effects of the housing crisis, any practice that serves to raise the cost of housing should be under the spotlight. If you have any monopoly tips or stories you'd like to share, drop us a line at hello@antimonopoly.ca

Follow CAMP on Twitter LinkedIn Instagram or Facebook |

Canada’s big media goes after OpenAI, while Ottawa targets Google

The Globe & Mail

On Friday, five of Canada’s major news media organizations, Torstar, Postmedia, The Globe and Mail, the Canadian Press and CBC, filed a lawsuit against ChatGPT creator OpenAI, accusing the generative AI company of copyright infringement. The Canadian Anti-Monopoly Project (CAMP) welcomed the Competition Bureau announcement, with executive director Keldon Bester saying in a statement that it represents a “turning point” for competition in Canada.

CAMP Celebrates Competition Bureau's Defense of Competition in Online Advertising

November 28, 2024 - After expanding its investigation into Google earlier this year, today the Competition Bureau announced that it is launching legal action against the company for abusing its dominant position in online advertising, inflating the cost of advertising and reducing the revenue going to publishers.

The Bureau alleges that Google has engaged in a range of anticompetitive conduct that has had the effect of cementing its dominant position in online advertising. The conduct includes unlawful tying of services, providing preferential ad inventory access to its own services, engaging in predatory pricing, and limiting how customers can interact with competing tools. To remedy the anticompetitive conduct, the Bureau is seeking an order that would require Google to sell off key parts of its online advertising business, its publisher ad server (DFP) and ad exchange (AdX), levy a financial penalty equal to three times the benefit gained from the anticompetitive conduct, and prohibit the company from engaging in anticompetitive conduct in the future.

In response the Canadian Anti-Monopoly Project (CAMP) released the following statement.

"The Competition Bureau's decision to pursue legal action against Google's dominance in online advertising represents a turning point for competition in Canada," said Keldon Bester, Executive Director of CAMP. "Online advertising is a critical tool for every Canadian business trying to reach their customers, and monopolization of this market means inflated costs that are ultimately borne by consumers. A monopolized online advertising market also means less revenue for the publishers and news ecosystem that keeps Canadians informed and supports our democracy. By challenging Google's dominance, the Competition Bureau is putting to work the new tools granted to the enforcer with unanimous support from federal MPs over the past year."

Additional materials related to the Competition Bureau's investigation can be found here

CI Financial signs $4.7B deal to be taken private by Mubadala Capital

The Canadian Press

Rachel Wasserman, a fellow at the Canadian Anti-Monopoly Project, said the widening net of private equity means there’s dwindling access to information on what these once-public companies are doing.

It also makes it harder for average investors to buy into the companies, and raises competition concerns as well. “When it’s one company, it doesn’t matter, but this is happening at such a scale that it is becoming a real problem,” said Wasserman, who wrote a recently published paper on the rise of private equity.

Letters: Hot Potato

November 24, 2024Welcome to Letters from CAMP, a newsletter on anti-monopoly activity in Canada and abroad, brought to you by the Canadian Anti-Monopoly Project. In this installment we have:

Let's dive in.

Canadian Potato Giants Caught Up in Cartel AllegationsFrozen fries, hash browns, and tater tots are at the center of a major antitrust controversy brewing in the U.S. but with potential implications for Canadians as well. Two Canadian companies - McCain Foods and Cavendish Farms - along with U.S.-based Lamb Weston and J.R. Simplot, are accused in two U.S. class-action lawsuits of orchestrating price hikes by sharing sensitive pricing data. These accusations are no small potatoes. In the U.S. these four companies control over 95% of the U.S. frozen potato market which generates $68 billion annually. The lawsuits describe "matching price increases" since 2021, allegedly enabled by data-sharing platforms and backroom coordination. The consequences of this conduct, if proven true, could have affected Canadian consumers as well. McCain is a true monopolist in the space holding nearly 80% of the frozen potato market in Canada, with Cavendish far behind with approximately 6% of sales. CAMP executive director Keldon Bester and antitrust expert and UOttawa law professor Jennifer Quaid appeared on Global News this week to discuss what the case might mean for Canadians. The case raises two important questions. First, how many more of these cartels are hidden in our economy? And second, how can we ensure fair outcomes for Canadians if regulators allow companies like McCain to become effectively a cartel of one? 👀 ICYMI 👀

Appointment Viewing: Trump 2.0 Lead Up Rolls OnThis week, CAMP executive director Keldon Bester took to the pages of the Globe and Mail to make the case for why Trump may not be all roses for big business. While reason for optimism exists, no one knows what Trump will do on the antitrust file, and the events of the last week have only further muddied the waters. The short-lived saga of now ex-congressman Matt Gaetz’s nomination as Attorney General brought a surreal mix of chaos and cautious hope. On one hand, the embattled former congressman—embroiled in ongoing scandals that have made the American payment app Venmo infamous—was hardly an ideal pick to oversee justice for corporate America. On the other hand, Gaetz was a relatively rare voice of genuine Republican support not only for FTC Chair Lina Khan but also a broader agenda skeptical of Big Tech and in favour of aggressive antitrust enforcement. The same cannot be said of Trump’s replacement nominee Pam Bondi, a former Florida Attorney General with a lobbying portfolio that includes Amazon and private prisons. Bondi’s appointment may shift the early tone of Trump’s second term, but it’s not clear that antitrust momentum is going anywhere. Trump’s first term launched the landmark Google search and Facebook monopoly cases, and skepticism of corporate consolidation remains bipartisan. Just this week, Republican Senator Josh Hawley grilled credit card executives, calling to “end the oligopoly” in payments amid the DOJ’s ongoing Visa-Mastercard investigation. As nominations and confirmations continue to shake out, Trump’s approach to corporate power remains a wildcard. But the antimonopoly movement is broader than a few federal appointments and extends far beyond the U.S. border. 📰 CAMP in the News 📰

U.S. DOJ Google Remedies Take Broad View of CompetitionThe wait is over for the U.S. Department of Justice’s (DOJ) proposed remedies to Google’s monopoly in online search. While headlines have focused on proposals to sell off the Chrome browser and end Google’s multibillion-dollar search deals with device makers like Apple, the DOJ’s proposed remedy takes a wide view of not only protecting competition today but the future of competition in markets tomorrow. The proposal includes important elements with the potential to spur competition in search, forcing Google to open up the index that powers its core search product, as well as providing greater transparency and control over data for the advertisers and publishers whose businesses rely on Google’s products. The DOJ also has its eye on competition in the emerging market for AI, requiring Google to divest any existing interests in potential competitors that could be used to co-opt competitive forces. With their broad scope, the DOJ’s proposed remedies aim not just to restore competition in search and advertising markets, but also emerging markets to which Google could extend its monopolistic reach. Now whether these remedies stick depends on not just the decision of Judge Amit Mehta, but also the resolve of the DOJ as the U.S. government enters a new era of leadership. If you have any monopoly tips or stories you'd like to share, drop us a line at hello@antimonopoly.ca

Follow CAMP on Twitter LinkedIn Instagram or Facebook |

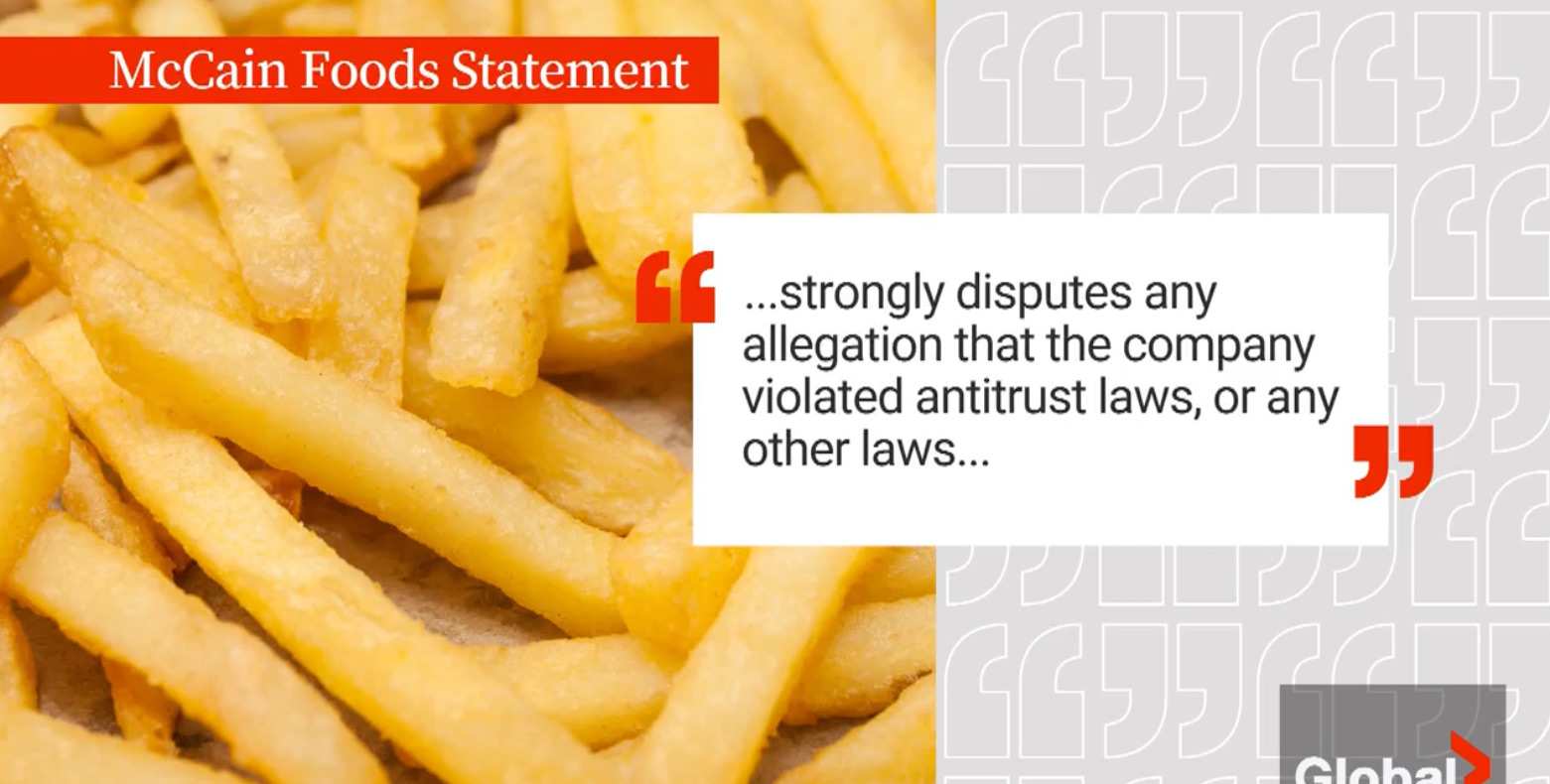

Two Canadian food companies sued in U.S. over ‘potato cartel’ allegations

Global News

In Canada, McCain Foods has even more dominance over the potato market, says Keldon Bester, executive director of the Canadian Anti-Monopoly Project, a think tank advocating for more competitive forces in the market.

On its own, McCain holds nearly 79 per cent of market share in Canada, with Cavendish holding roughly six per cent, according to 2020 figures from Agriculture and Agri-Food Canada.